Prepare For The Earnings Week Ahead

← Retour au Tableau de Bord

Published: July 13, 2026

URL YouTube

https://www.youtube.com/watch?v=TPjLjj1NLpA

Statut

Analyzed

Demandé Le

July 14, 2026 at 06:02 AM

Performance Globale

En attente

Recommandations

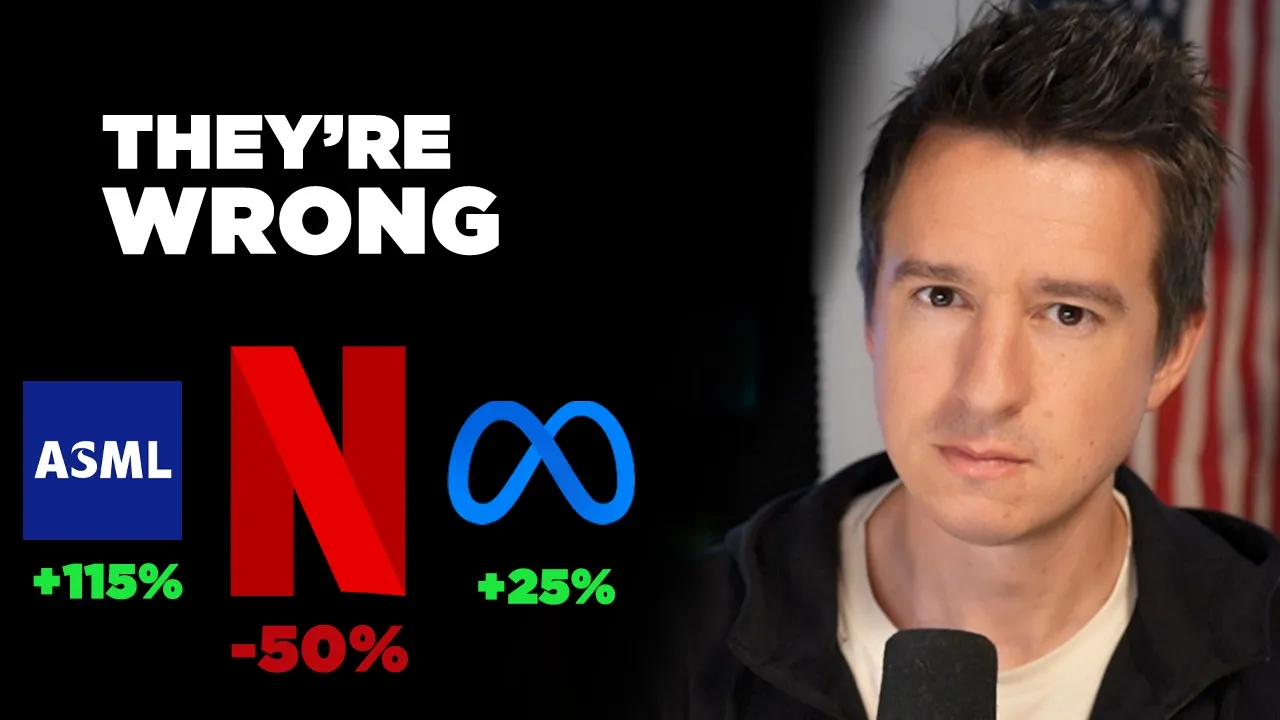

NFLX

BUY

"if there's any weakness in the stock in the meantime, I'm going to be buying it. If Netflix drops from the 70s into the 60s, I'll be once again increasing my stake in the company."

Contexte: "If there's any weakness in the stock in the meantime, I'm going to be buying it. If Netflix drops from the 70s into the 60s, I'll be once again increasing my stake in the company."

Prix à la date de publication: $73,83

Prix de clôture du dernier jour: $73,83

(Jul 13, 2026)

Bénéfice/Perte:

+$0,00

(+0,00%)

ASML

SELL

"I've made two trims of ASML. Both of them around one around $1,900 per share, the other around $1,750. And I trimmed both of these because I believe that ASML has ran up a lot."

Contexte: "Over the past month, I've made two trims of ASML. Both of them around one around $1,900 per share, the other around $1,750. And I trimmed both of these because I believe that ASML has ran up a lot."

Prix à la date de publication: $1 726,04

Prix de clôture du dernier jour: $1 726,04

(Jul 13, 2026)

Bénéfice/Perte:

+$0,00

(+0,00%)

Transcription Complète

We find ourselves once again at quarter end, the time of the season where accountants have been crunching the numbers and working overtime. This week we have a number of important industries and companies reporting earnings. First of all, we have JP Morgan with the rest of the big banks, Bank of America and Goldman Sachs. Then we have ASML and TSM also reporting earnings this week. The two semiconductor companies are expected to do phenomenally well with the increased demand we've all seen in the market. But is this market tapped out on these type of companies? have we finally reached a breaking point on ASML or TSM. We'll be looking at that. And then we also have on Thursday Netflix reporting earnings aftermarket close. Netflix is central to a lot of discussion today because the stock has plummeted 50% from its highs from $140 down to $70. It looks like it could go into the 60 range. There's reports and many indications that Netflix is lacking in engagement and content. They've tried to buy companies like Warner Brothers Discovery and they opted out of the deal. Now it looks like they're trying to do whatever they can to keep engagement going. As a Netflix investor, I'll be going over the situation here along with a lot of deep dive analysis on really what's going on with Netflix and if investors should be concerned or if now is a buying opportunity. We also have this week a lot of other news. For example, Meta is up 21% in 15 days. Why the sudden change in sentiment for Meta? We also have Apple suing OpenAI alleging they stole trade secrets and we have a number of states including California suing Paramount over their proposed merger. So we have a ton to get to in this episode and we start things off today talking about Netflix. If we look at the week overall we have a number of companies reporting their earnings but Netflix is going to report like we said right here Thursday after market close. The reason that I want to focus on this one is because Netflix is embroiled in a lot of controversy. This controversy has caused the stock to drop precipitously over the past couple of months. It has been a continual decline day after day. Netflix stock today trades at $744. In late 2025, Netflix was at a high, trading near $140. Netflix is also recently growing faster in the aggregate of the S&P 500, and it's growing its margins, its earnings, and its revenue faster. The Wall Street Journal has this article that highlights the conundrum that Netflix is in. They say that late last year profits were rising. Consumer defections remained at industry lows. That's the churn rate. It's super low for Netflix. And it had hit franchises including Bridgetgerton and Stranger Things. But one metric was pointing in the wrong direction. Subscriber engagement was showing signs of decline according to attendees. At the time, it was a small part of the conversation about the company's goals, but it has since become a frequent topic of discussion at meetings. So management's feeling good saying we have these hit shows and industry low churn, but they're also noticing that people are spending a little less time watching shows and completing shows. We saw the report from Bloomberg that Netflix has this problem where people start season 1 and then they lose half the viewership when they get to season two. Trying to figure out why that is is difficult. There's lots of metrics going on, but for whatever reason on Netflix, people are far less likely to finish multiple seasons. Now, this small problem has grown into more of a main talking point. To bolster engagement, executives at the company have recently discussed adding live channels that would continuously stream certain programs or shows and films from certain genres according to people familiar with the matter. Uh-oh. They're going to be adding live channels that would continuously stream certain programs. So, cable television, that doesn't look good at all. And this is why investors are concerned about Netflix. no big hits, people having trouble finishing season two or season 3, and then you have reports that they're literally turning into cable. They're going to have cable television channels just constantly playing content. Then to add insult to injury, this just gets worse. They say the company has also explored bundling other subscription-based streaming services, including NBC Universal's Peacock, into its offering. Now, Netflix is becoming more complicated, talking about bundling services. Netflix's discussions about adding TV channels and potentially streaming bundles, which would appear like tiles on the streamer's homepage, show how the company's willing to pivot from its roots. This goes against everything that Netflix stood for over its history. The CEO of the company, Reed Hastings, preached the importance of focusing on simplicity to succeed. But Netflix now faces increased competition from the likes of Disney, HBO Max, YouTube, free and adup supported streaming services such as Fox Corpse, Tuby, and the Roku channel. They all include linear channels and are known for more casual viewing than Netflix, and they're gaining viewership fast. So, while all of this is going on, we're in a market that's heavily driven by story and narrative. Story is what causes stocks to go up or down today. If you can convince investors to believe that your company has a great story, the stock will go up. Fundamentals play a role, but they only play a role over the very long term. Right now in 2026, the story is the dominant force. With Netflix, right now, the story is being dictated by the media and these external reports. We have increased competition, all the dynamics changing in this media landscape. We have companies like Instagram and Meta competing for your time, for your engagement. And then we have Netflix which looks desperate by constantly changing their business model and expanding what type of things they're doing. But I believe overall as we look at this that this portrays Netflix in a far more desperate and I believe weak position than they're actually in. I think the situation that Netflix is in is actually very advantageous, a very advantaged company right now. If we look at what Netflix is actually doing, I believe it follows in the path of what they have been doing for a long period of time. Netflix has constantly been adding on new sources of content. They've been doing this since the beginning. Netflix started off by basically licensing competitors key series like Parks and Wreck in the Office. Licensed shows from NBC and Disney. They would put them on their service and make it so you could binge them and just watch them continuously. But then Netflix decided to make their own core content. They made Orange is the New Black. They made House of Cards. They made lots of good series that were Netflix originals. So they expanded what they were doing. They offered new content. You could have said that's out of desperation. It was, but it worked. And the Netflix membership became more valuable. People were even less likely to turn or to cancel their membership because they weren't reliant solely on licensing content. But Netflix didn't stop there. They kept expanding the type of content that they offer. They went into documentaries. Netflix started to make so many documentaries and they stole that category from HBO. HBO up until that point had the really premium documentaries, but Netflix got it down. They got the recipe down. Their documentaries are extremely good. So Netflix has this entire documentary flywheel. Very engaging, interesting stories that they tell at a very low cost. Netflix decided not to stop at documentaries. They went for stand-up comedy. They started to license the biggest, most relevant comics, stealing that industry again from HBO. So Netflix has been continually expanding its entire catalog and the types of content that it creates over and over again. Netflix decided to expand big into Korean content. There's so many Korean shows on Netflix and that's been a massive demographic both in South Korea and outside of it. Netflix has expanded the type of shows it's done from sitcoms to very highbrow intense uh thrillers and different shows. They've experimented in blockbuster movies and comedies and so on. Netflix is a company of constant expansion. When we look at what they're doing more recently, they've also expanded into taking YouTubers. People like Mark Robber, they take some of their series and they put it in the kids section. So, they have quality kids content to watch. They're doing more of that where they're taking do-it-yourself content creators and putting on the Netflix platform. Netflix also tried to get Mr. Beast. They were outbid by Amazon Prime. They did so with live television as well. Live events like Alex Honold climbing the skyscraper. you have sporting events, the Christmas Day NFL games, and so on. The story here is one of massive content expansion over time. So, when I see reports that Netflix is expanding into podcasts, I read that as just one more expansion. Netflix is doing the same thing with podcasts that they've done throughout their entire lifetime. They're expanding the type of content they offer. Then we look at the concerns about Netflix potentially having continuous channels playing like cable television. This is something that is way overstated by the Wall Street Journal and other news outlets. Netflix has actually looked at this idea for years. So this whole thing of becoming cable television and having continuously playing channels, that's an idea that Netflix has mold over for literally five plus years. They've looked at that over and over again. They have different interfaces built to test it out. The way that Netflix looks at that is it would be a tool to break indecisiveness. Meaning when you log into Netflix, instead of being forced to pick what you want to have play, it might be interesting to just show you something already playing and you can go, "This looks interesting. I'm going to continue watching." So, it's just a different way to deliver the same content. Also, if Netflix did have continuously playing channels like cable television, it would be different than cable television because it would only be Netflix's content. It wouldn't be any type of external content. and it would just be their shows and specific made channels that are already playing. That's very different than what the media is trying to portray. Now, in terms of the concerns in the reports about engagement and the issues Netflix is facing with engagement, I believe they're very real. I think Netflix is facing an engagement problem. They say in their report that their internal quality engagement metric hit an all-time high in Q1. That's true. But if they're starting to see a little bit of deterioration, a little bit less watch time, that is going to alert Netflix managers. They're going to look at that and see that they have an issue that needs to be addressed. But addressing issues is what Netflix does. They do this all the time. The issue that they addressed back in 2022 was that subscribers were going down. They surely addressed that. It went up 70 million since then. The issue they're addressing now is engagement, and they're going to do everything they can to address it. The advantage state that Netflix has is that they have 325 million subscribers, growing revenue, they have very low churn. They have a membership that offers a great deal of current value. So, if they're seeing engagement go down, they're going to work overtime to figure out ways to fix that. They're going to look at different engagement hooks, different ways of displaying content, creating content, releasing content. It's likely that Netflix will have eventually another big hit again. They usually don't have a a drought of hits that often. And I believe that they will work overtime to fix this. Netflix is a company that has continually changed and pivoted and adapted. One of their biggest strengths is their management. They're extremely technologydriven, data driven, flexible. They have an incredibly good core infrastructure to be able to pivot on a dime and fix any problem within the company. So, while there's reports of engagement, I believe those are real. I do have a belief that Netflix can address them and fix them over time. So, in terms of this earnings report this week for Netflix, this will be front and center. What does their engagement look like? What are people looking at with the content? Are they losing market share? Those are the type of questions that they're going to be asked. I believe that Netflix will do whatever it can to address this issue, but this earnings report may not show that. It takes time to make adjustments and increase engagement in an application like Netflix. Even creating content, the life cycle of that takes a lot of time. So, if there's any weakness in the stock in the meantime, I'm going to be buying it. If Netflix drops from the 70s into the 60s, I'll be once again increasing my stake in the company. Now, next we get to Meta. Meta's not reporting earnings this week. In fact, they're reporting later this month, but I believe it's relevant to bring up today because Meta has been under a lot of controversy, a lot of opinions about this company. It's a stock that I'm very bullish on. So, I have a Meta position here. It's one of my largest positions and it's currently in the red, but only by a fraction. Meta was down $30,000 at one point. So, we were down pretty deep in the red on it. Now, it's down $6,000 or 3%. It's a $176,000 position. So, Meta has really come back. In fact, in the past 15 days, it's up 21%. So, this massive company has gone through a huge run over a very short time period, and that's because of this post right here. Now Mark Zuckerberg once again just in the past week took to X to post about a new Muse model. This is their AI model. He says quote today we're releasing Musepark 1.1 a strong agentic and coding model at a very low price. It's available through the new meta model API and in meta API. Musepark 1.1 is the strongest at agentic performance tool use and computer use. It does well on longunning tasks with 1 million token context windows. It can delegate execution to sub agents running in parallel and is trained to use computer interfaces on desktops, mobile and browser. Now, if we look at what Meta is trying to do here, investors are excited that Meta is offering a highly competitive and cheap model. And that makes sense because that's Meta's goal. Meta's goal is to bring down costs and make it so that AI models are not all that unique. They're not that great of a business model. they really want to break flagship models as a business to begin with. And this is where we get into the different motivations for all these different AI companies. So I created something that I think will help frame this. This is the motivation framework. If we look at all the big AI companies that have their own models, we have uh Metahare, Google, Amazon, OpenAI, and Anthropic. These are the ones that we can include. There's other ones as well, but these are are five that I think are are the most meaningful here. When we look at this, I think it's important to understand where their motivations lie. They have different degrees of how commoditized or uncommonized they want their AI model to be. In the case of Meta, they want AI models, the entire model layer to be as commoditized as possible. Commoditized meaning interchangeable, indistinguishable, doesn't matter which model you use. They want to they just want to bring down costs and make models as a thing as cheap and as accessible as possible. That is Meta's goal. That is their motivation. Now, why is that Meta's goal? Because Meta is in a unique position where they do not need charging for the model to be their monetization layer. Their monetization layer is their massive distribution. All of their glasses, all of their personal assistants, their 3.5 billion daily active users on Instagram and Snapchat and Facebook threads. you name it. They have so many users on so many different applications from the Facebook marketplace to Instagram and and uh reals every single day. Meta has a million plus ways to monetize through AI without charging for it. So Meta's goal is to bring down costs, monetize through massive distribution. They're making their products more efficient. They're making it so that you have personal assistance, making it so that there's not any one company that controls the AI layer. They don't want everybody to be beholden to an anthropic or an open AI having to go through those gatekeepers. They want to be vertically integrated, control the entire stack, and monetize through billions of users and trillions of interactions every single day. That's Meta's goal. So Meta has the motivation of highly commoditized. Google I think is in between. I put them as partially commoditized, partially premium. So Google shares a lot of the attributes of Meta. They have the distribution layer, the billions of users, the tons of apps to monetize from. They want the unit cost to be very low for AI. So they're working towards that. But they also want to have a little bit of a premium part as well where they charge for their AI model. They want it to be distinguishable and to be uh have a premium price attached to it. So I think that Google and Meta are relatively close. They're mostly going to monetize through their massive infrastructure distribution and vertical integration. Amazon also wants the AI unit cost to be extremely low. They want the AI model to be competitive and interchangeable. They're not really focused on making their own. They just want everyone else's to be competitive and interchangeable. And I believe that Microsoft fits firmly in the same category as Amazon. So you could say Amazon or Microsoft here. They're going to be monetizing AI through AWS infrastructure through offering everything inhouse as the hub themselves as Amazon already does. So these three companies, Meta, Google, and Amazon, mostly want to monetize through either competitive interchangeable models, distribution, cloud hosting, or all of their their their massive platforms that they offer. When we get to OpenAI and Enthropic, their motivations are entirely different. They both want their model layer to be premium and defensible to be highly unique. They want AI costs to go down, but they also want them to be highly differentiated so that they can continue to charge directly for their APIs so that people have a reason to pick Open AI over Anthropic. They want differentiation where Meta, Google, and Amazon don't want differentiation. The way that OpenAI and Enthropic want to monetize is through APIs, agents, subscriptions, and enterprise agents. They want their model to be the monetization layer. These businesses are at odds with each other's motivations. The hyperscalers have different motivations than the OpenAIs and Enthropics. And I believe in this tugof-war, the companies that will ultimately win out are the hyperscalers, the Meta and Google and Amazon. It'll take time, but I believe firmly that over time models will become cheaper and cheaper and less and less differentiated. If we have companies like Meta investing hundreds of billions of dollars into core infrastructure, Meta has endless compute power, endless money to spend on this, they can make their models as good as OpenAR Enthropic over time. And Meta is on the heels of these flagship models already with a short amount of time. Give it a couple years and I believe it will become even more difficult to distinguish between one model or the next. And in that case, when you can no longer distinguish between one model and the next, the companies with the motivation of commoditizing the models wins. Now, going through this week, we also have JP Morgan, we have ASML, and we have TSM. I'll first start off with JP Morgan and the big banks. Simply put, I think these earnings are going to be really good. These companies make a lot of money from trading activity, and the market has been highly volatile. traders have have bet heavily on these companies. I think that they're going to be doing really well in their trading floors, in their investment activities, the investment services. I also believe that their credit card portion of the companies will do really well. JP Morgan makes a lot of money from Visa, huge amount of money from credit card activity. All the big banks sign up with one of the cards, Visa, Mastercard. I believe all of them are doing really well. And these companies do well with higher interest rates, which have actually held up. Interest rates haven't been plummeting. So overall, I believe the big banks are going to do well. ASML over the past year and a half has been in an incredible position. Along with TSM, these companies have raced upwards with all the semiconductor hype. It's currently $122,000 position, $90,000 in the green. So it's been a massive winner in the portfolio along with Google for the past year. But over the past month, I've made two trims of ASML. Both of them around one around $1,900 per share, the other around $1,750. And I trimmed both of these because I believe that ASML has ran up a lot. The valuation has climbed. And even though I believe that fundamentally speaking, the company's great and the moat continues to be extraordinary, I believe it's warranted to take some off the table when you see valuations rise this high this fast. If we look at ASML, it's now at a 45 PE ratio. That's very high. Even for a company as good as ASML, this is still a somewhat cyclical company. It's not as cyclical as memory or any of them, but it does have some cyclical demand. And ASML is trading at a super high valuation, lots of gains in a short amount of time. And I believe it's just prudent to take some money off of the table, especially when there's so many other companies offering great opportunities. We have companies like Uber and Netflix and Meta that are all great at much lower valuations than ASML. Now, I've been signaling this for a while. For the past month or two, I've been saying that I believe there's going to be a slowdown in the semiconductor trade. I believe that momentum will eventually fade. Stock prices are super high. Margins are very high. And there's a lot of mechanics that make me believe that things will slow down and turn to other companies. If the market narrative shifts towards buying other highquality, durable growth companies at low valuations, then my portfolio is well prepared. So, while I'm still very bullish fundamentally on ASML and TSM, I'm not making any big bets on them this quarter. They could go up 10 20%, we could see another bit of momentum in them. I'm sure the reports are going to be great, but I'm actually in the position right now of trimming and shifting the portfolio towards the quality growth companies at low valuations than I am piling more into semiconductors. Now, moving on from this earnings week, we do have some massive stories to get into. First of all, Paramount Warner Brothers Discovery is being hit with a massive lawsuit. It finally it finally happened. 12 states are suing them, including California, to block the merger. The attorney general of California is suing them with 12 other attorney generals challenging the 110 billion dollar acquisition. To summarize their arguments, and we could go into it. We have the the whole thing here. It's 100 pages plus long. But if we look at the key points of it, it's the type of things you would expect. They outline first and foremost that unlike Netflix, which had no box office business, Paramount already has one. And then they're buying Warner Brothers Discovery, which already has a big one. So they're combining two box office businesses together. Both Warner Brothers and Paramount are two of the five major film distributors and will combine around 20% 27% share of the market. After the merger, only three distributors will control 75% of these films and only four distributors uh with defendants Disney, Universal, and Sony will control 86% of them. So they're highlighting market concentrated power in film distribution. Now the arguments go into much more detail on the lawsuit. They have every metric and number you can imagine. But when I look over all of this, I still think it's unlikely for these states to succeed. For example, the biggest thing that is a problem to these states suing Paramount is the fact that the Department of Justice has already looked deeply into the same exact thing and came to the exact opposite conclusion of these states. And there's a lot of arguments that I believe are actually actually more solid from the Department of Justice. For example, they point out that in the box office, categorizing market share is highly volatile. One box office distributor might do really well one year, they have a big film like Oenheimer, right? They might do really well that year, then the next year they may not have a big mega hit. Or there's a couple years where Disney did really well with Marvel shows, now they're not quite as popular. The Supergirl has been a flop in the box office. So things change yearbyear. the market share is not some continuous thing like it is in cable television. So there's a lot of arguments to the other side. The Department of Justice has already said these things aren't really an issue and I believe that Paramount is going to get this past the state suing them. Now finally we get to the fail of the week which there's a lot of failing going on in this one. We have first of all Open AI stealing documents from Apple. Now this isn't one of those cases where I mean they took like a couple documents and Apple's just freaking out and overreacting. No. An employee that worked at Apple that moved to OpenAI systematically with full intent and motivation over weeks of time stole incredible documents from Apple. Incredibly detailed designs of basically all their hardware. Apple has responded with a thermonuclear lawsuit. Steve Jobs declared thermonuclear war on Google's Android operating system back in 2010, calling it a stolen product. Now his successor is going to battle against Apple's new and dangerous rival. Tim Cook fired a missile at OpenAI. In a lawsuit filed Friday, Apple alleged that the senior OpenAI executive once sat at top Apple's own product design team was involved in a monthslong campaign to steal Apple trade secrets. A spokesperson from OpenAI didn't directly deny it, but they just said that they have no interest in stealing trade secrets from other companies. Sam Alman said on Twitter that he's not afraid of Apple and he respects them. It's what he said. Now, there is a lot of evidence to support this from what I've seen. The documents are extremely extensive and what OpenAI has done here. But what Apple's strategy is is to leverage this theft of IP to put OpenAI in a legal jail for as long as possible, making it so that they cannot release hardware. Apple in essence is looking to exploit this decision from OpenAI and use it to their advantage. If they can make it so Open AI can't develop any type of hardware for as long as possible, that's good for Apple. And aside from what you may actually believe, Apple does consider OpenAI a very real threat when it comes to hardware. They know they're working on it. They know they have good AI models. They know they'll likely come out with good devices. So, Apple's treating this like a very real threat, and they will wrap up Open AI in legal purgatory for as long as possible. Now, of course, this is a feud between Apple and Open AI, Tim Cook and Sam Alman. But Elon managed to find a way to put himself at the center of this feud as well, as he often does. In this case, he just commented simply on Sam Alman. He called him scam Altman. And he says in this post here, "Scam Altman is super good at scamming." That's an old tweet before this came out. And then Elon Musk replied to that. He posted it again saying he takes scamming to a whole new level. Then the billionaires started bickering, which you may believe that it's Elizabeth Warren or AOC or Mandani or Bernie Sanders that hates billionaires more than anyone else, but you'd be wrong. Nobody hates billionaires more than other billionaires. We have Sam Alman responding to Elon Musk's criticism, saying, "Homeboy, you're the one selling public market investors on short-term space data centers." So, he's taking a jab at Elon Musk SpaceX and their plans to put data centers in space. Sam Alman calls him homeboy. That that's that's real. He called him homeboy. Elon Musk replies to this and says, "We start flying them next year. Maybe you can come see them if your parole officer approves." It's just it's just great. I love reading this stuff. I love how much they hate each other. I don't know why. It's like they both could just be on an island enjoying their life with their family, but they choose to be on having petty arguments like anyone else online. It's just amazing. It shows that no matter how much money you have, it can't it doesn't change these things, and it it's incredible to see. After stealing an open- source AI charity, you then stole all of Apple's phone technology. Wow. What do you plan to do for an encore? That's tough to beat. Elon Musk, great tweet here. Sam Alman's was was pretty good as well. But Elon Musk, I I really think had the better he got the better exchange here. Just a better tweet. Sam continued to poke the bear on Elon Musk's own platform, saying, quote, "There are a lot of benchmarks that suggest 5.6 six soul is the best model in the world right now. But the most reliable way to tell is that Elon is obsessed with me. Again, that's a pretty good rebuttal from Sam. Sam has continued to express his skepticism of Elon Musk's space data centers. >> With the current landscape of putting data centers in space is ridiculous. It will make sense someday. But if you just do like the very rough math of launch costs relative to the cost of power we can do on Earth to say nothing of how you're going to fix a broken GPU in space and they do break a lot still unfortunately. We are not there yet. There will come a time space is great for a lot of things. Orbital data centers are not something that's going to matter at scale this decade. He says orbital space centers aren't even going to matter this decade. And then he doubles down on a different podcast saying essentially the same thing. >> Meaningful amount of compute for open AI in the next 2 to 3 years, 5 years. >> No, >> 10 years. >> Um, >> you just keep going. 10,000 years. >> I I wish Ethan luck. >> Okay. So, we can enjoy seeing these two continue to bicker back and forth with each other, proving that no amount of money can buy you class or solve most of life's problems. That's going to be it for this episode. See you in the next one.