My Investing Plan For The Next 5 Years

← Retour au Tableau de Bord

Published: May 26, 2026

URL YouTube

https://www.youtube.com/watch?v=yzplj-RvvBw

Statut

Analyzed

Demandé Le

May 27, 2026 at 06:00 AM

Performance Globale

+4,51%

Recommandations

ASML

BUY

"I think you should own some companies from phase 1. For example, I chose ASML."

Contexte: I want to reiterate that this doesn't mean that every company from phase 1 will do poorly. And I also want to reiterate that I think you should own some companies from phase 1. For example, I chose ASML.

Prix à la date de publication: $1 632,03

Prix de clôture du dernier jour: $1 804,25

(Jul 10, 2026)

Bénéfice/Perte:

+$172,22

(+10,55%)

GOOG

BUY

"the phase 3 winners, the buyers of AI, specifically Google, Microsoft, Amazon, and Meta. I have made these four companies in particular the biggest bets in my portfolio."

Contexte: But where I have most of my exposure and where I believe that the long-term predictable gains mostly reside are in the phase 3 winners, the buyers of AI, specifically Google, Microsoft, Amazon, and Meta. I have made these four companies in particular the biggest bets in my portfolio.

Prix à la date de publication: $384,84

Prix de clôture du dernier jour: $356,24

(Jul 10, 2026)

Bénéfice/Perte:

$-28,60

(-7,43%)

MSFT

BUY

"the phase 3 winners, the buyers of AI, specifically Google, Microsoft, Amazon, and Meta. I have made these four companies in particular the biggest bets in my portfolio."

Contexte: But where I have most of my exposure and where I believe that the long-term predictable gains mostly reside are in the phase 3 winners, the buyers of AI, specifically Google, Microsoft, Amazon, and Meta. I have made these four companies in particular the biggest bets in my portfolio.

Prix à la date de publication: $416,03

Prix de clôture du dernier jour: $384,36

(Jul 10, 2026)

Bénéfice/Perte:

$-31,67

(-7,61%)

AMZN

BUY

"the phase 3 winners, the buyers of AI, specifically Google, Microsoft, Amazon, and Meta. I have made these four companies in particular the biggest bets in my portfolio."

Contexte: But where I have most of my exposure and where I believe that the long-term predictable gains mostly reside are in the phase 3 winners, the buyers of AI, specifically Google, Microsoft, Amazon, and Meta. I have made these four companies in particular the biggest bets in my portfolio.

Prix à la date de publication: $265,29

Prix de clôture du dernier jour: $247,04

(Jul 10, 2026)

Bénéfice/Perte:

$-18,25

(-6,88%)

META

BUY

"the phase 3 winners, the buyers of AI, specifically Google, Microsoft, Amazon, and Meta. I have made these four companies in particular the biggest bets in my portfolio."

Contexte: But where I have most of my exposure and where I believe that the long-term predictable gains mostly reside are in the phase 3 winners, the buyers of AI, specifically Google, Microsoft, Amazon, and Meta. I have made these four companies in particular the biggest bets in my portfolio.

Prix à la date de publication: $612,34

Prix de clôture du dernier jour: $631,48

(Jul 10, 2026)

Bénéfice/Perte:

+$19,14

(+3,13%)

AMZN

BUY

"Amazon and Meta are my two top picks this year."

Contexte: Google has to compete with chatbt. Microsoft has to deal with claude within its business. Uh Amazon, I think actually Amazon is in a great position. Amazon and Meta are my two top picks this year.

Prix à la date de publication: $265,29

Prix de clôture du dernier jour: $247,04

(Jul 10, 2026)

Bénéfice/Perte:

$-18,25

(-6,88%)

META

BUY

"Amazon and Meta are my two top picks this year."

Contexte: Google has to compete with chatbt. Microsoft has to deal with claude within its business. Uh Amazon, I think actually Amazon is in a great position. Amazon and Meta are my two top picks this year.

Prix à la date de publication: $612,34

Prix de clôture du dernier jour: $631,48

(Jul 10, 2026)

Bénéfice/Perte:

+$19,14

(+3,13%)

SPGI

BUY

"I've personally chosen S&P Global and Moody's."

Contexte: Out of these ones, I've personally chosen S&P Global and Moody's.

Prix à la date de publication: $412,48

Prix de clôture du dernier jour: $435,01

(Jul 10, 2026)

Bénéfice/Perte:

+$22,53

(+5,46%)

MCO

BUY

"I've personally chosen S&P Global and Moody's."

Contexte: Out of these ones, I've personally chosen S&P Global and Moody's.

Prix à la date de publication: $451,10

Prix de clôture du dernier jour: $487,02

(Jul 10, 2026)

Bénéfice/Perte:

+$35,92

(+7,96%)

UBER

BUY

"I think Uber and Door Dash will be spectacular winners."

Contexte: We also have companies that are at some risk in some aspects of AI, but overall they have a lot of nonAI aspects, and I'd put Uber and Door Dash in that category. I think Uber and Door Dash will be spectacular winners.

Prix à la date de publication: $70,12

Prix de clôture du dernier jour: $74,35

(Jul 10, 2026)

Bénéfice/Perte:

+$4,23

(+6,03%)

DASH

BUY

"I think Uber and Door Dash will be spectacular winners."

Contexte: We also have companies that are at some risk in some aspects of AI, but overall they have a lot of nonAI aspects, and I'd put Uber and Door Dash in that category. I think Uber and Door Dash will be spectacular winners.

Prix à la date de publication: $154,00

Prix de clôture du dernier jour: $192,35

(Jul 10, 2026)

Bénéfice/Perte:

+$38,35

(+24,90%)

SHOP

BUY

"I think that Shopify is a spectacular winner."

Contexte: I think Uber and Door Dash will be spectacular winners. I think that Shopify is a spectacular winner.

Prix à la date de publication: $104,90

Prix de clôture du dernier jour: $123,17

(Jul 10, 2026)

Bénéfice/Perte:

+$18,27

(+17,42%)

ABNB

BUY

"I think that Airbnb will do really well."

Contexte: I think that Shopify is a spectacular winner. I think that Airbnb will do really well.

Prix à la date de publication: $132,68

Prix de clôture du dernier jour: $146,89

(Jul 10, 2026)

Bénéfice/Perte:

+$14,21

(+10,71%)

SPOT

BUY

"I believe that those will end up being differentiated and be rerated higher as well."

Contexte: We even have companies that there's a bit more debate about companies like Spotify and Dualingo. ... So I believe that those will end up being differentiated and be rerated higher as well.

Prix à la date de publication: $529,71

Prix de clôture du dernier jour: $485,22

(Jul 09, 2026)

Bénéfice/Perte:

$-44,49

(-8,40%)

DUOL

BUY

"I believe that those will end up being differentiated and be rerated higher as well."

Contexte: We even have companies that there's a bit more debate about companies like Spotify and Dualingo. ... So I believe that those will end up being differentiated and be rerated higher as well.

Prix à la date de publication: $106,48

Prix de clôture du dernier jour: $129,95

(Jul 10, 2026)

Bénéfice/Perte:

+$23,47

(+22,04%)

RACE

SELL

"some investors are deciding to sell out of the stock."

Contexte: Investors are trading the company down. It's down 5.7%. So, some investors are deciding to sell out of the stock.

Prix à la date de publication: $329,91

Prix de clôture du dernier jour: $375,03

(Jul 09, 2026)

Bénéfice/Perte:

$-45,12

(-13,68%)

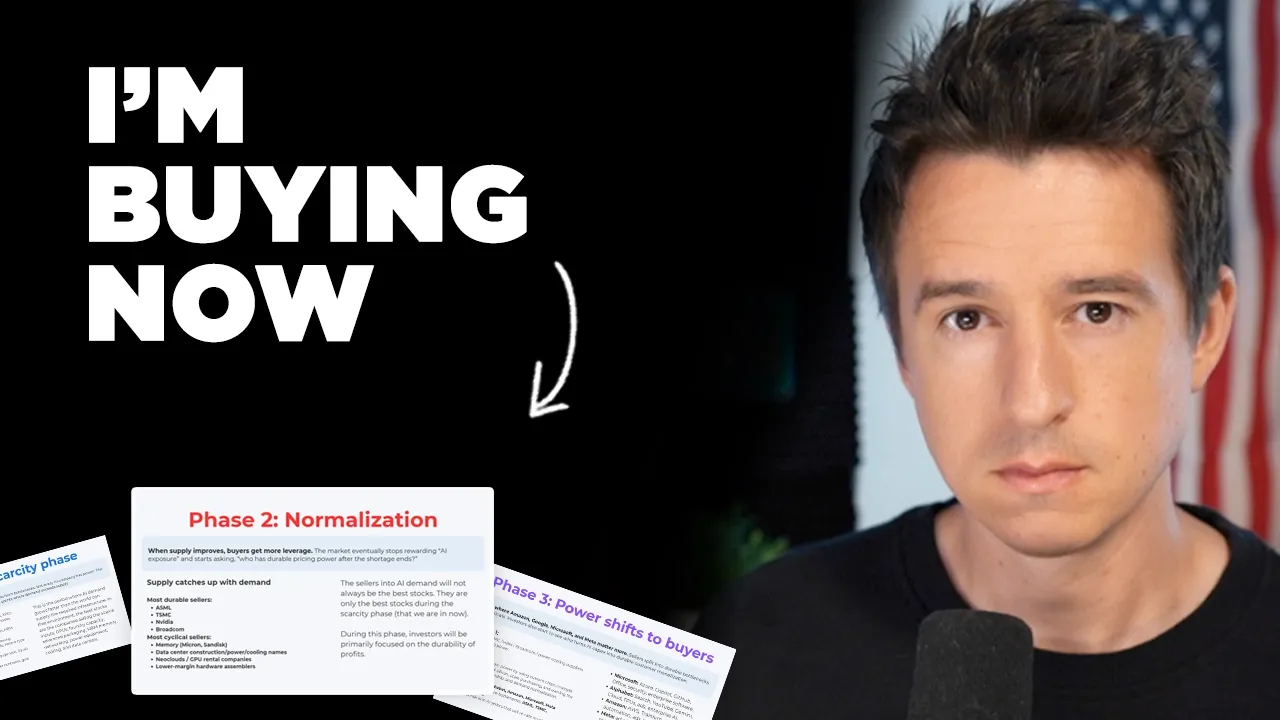

Transcription Complète

There's so many questions revolving artificial intelligence. Which companies are going to benefit from this? We've already seen that many of them have. Micron Technologies just surpassed a trillion dollar market cap. Can it go on? Have things changed? Will it go back down? We also have software companies, ones like Adobe and Salesforce and into it going way down. Will they stay down forever or are they going to have a resurgence? We have the big tech leaders. We have the Nvidias and the Microsofts and the Amazons. What's going to happen with these companies over the next five years? Well, that's what we're going to be discussing in this episode. I'm going to give you my AI road map and how I believe everything will evolve over the next 5 years. I'll even be walking you through this road map with four different phases. We have phase one, the one that we're in now, the scarcity phase. We have phase two, normalization, and then of course, we have phase three and phase four of how things will evolve over the next 5 years. and I'll be going over it in detail, showing you exactly what I think is going to happen and which companies will be the winners and the losers in the process. I'll be going over how I'm positioning my portfolio to take advantage of this in the best riskadjusted way possible. So, we have a ton to get to. It's going to be a lot of fun. Plus, we have a lot of news to get to. For example, Ferrari introduced an EV. It's not being received well. And in today's fail of the week, we have the cancellation of Steven Cobar's Late Show. It's come to an end and a lot of people are blaming Trump, but Trump is actually not the problem here. The problem is YouTube. We'll be discussing in this fail of the week. So, we have a ton to get to in this episode. Let's go ahead and jump in. Now, we start things off today by going over this AI transition. This is, after all, one of the biggest transitions the market has ever faced is the advent of AI and its unprecedented adoption. We've already seen the incredible impacts this has had on many industries from all the hardware sellers to all the software companies going down and and everything else in between. And investors are trying to make sense of all of this. Now, a lot of investing comes down to doing individual stock research. So, you're looking at a company, you're looking at the fundamentals and the revenue and trying to see if this company's a good bet for the next 10 years. And although I think that's great to do all that fundamental individual groundup research, I also think it's good once in a while to take a step back and look at overall what's going on. And that's what we're going to be doing here. So I want to start things off by looking at what I believe we're in right now, which is phase one. Phase one, again, this is what we're in today is the scarcity phase. AI infrastructure sellers win. This is something that Katau management highlighted that there are sellers of AI and buyers of AI. The sellers of AI are the ones selling into the demand of AI. They're selling into scarcity. Power comes from bottlenecks. Pricing power comes from bottlenecks. If you have a product that a lot of people suddenly want all at the same time, it gives you immense pricing power. See, not every AI company has power. The companies with the power are the ones sitting at the point where demand exceeds supply. right now that is the accelerators. Nvidia GPUs, custom A6, XPUs, any company in this category have incredible power. Nvidia has incredible pricing power today because of course it's a huge it's a huge bottleneck. We even look at Nvidia's most recent report and the revenue is growing like 80% year-over-year even today. That is absolutely insane. And that is again part of this because of scarcity. We have foundry capacity that's TSMC leading edge nodes. You have immense power today. One of the most important companies on planet earth. Immense pricing power. And then of course we have ASML. Now this is a stock that I own within these sellers. These are the ones selling into the AI scarcity. ASML of course is a a massive bottleneck. It's an outright monopoly making the EUV machines. It sits there is a critical part of advanced chip manufacturing. Without it, you can't really make anything. So they have immense pricing power. We have advanced packaging, chiplets, HPM integration and so on. We have HBM Memory, SKH Highix, Micron, and Samsung. Micron literally today just surpassed a trillion dollar market cap going up 18%. Over the past year, the stock is up like 10x because Micron is selling memory. All of a sudden, everybody wants memory. We have networking Broadcom Arista Credo a stereotype connectivity. All these companies massive winners into this selling into the AI demand. The number seventh level beneficiary here are the powering and cooling companies. Vertive electric equipment, uh, liquid cooling. Any company that specializes in cooling down these large data centers of course is incredibly incredibly powerful today. They have immense pricing power because everybody suddenly needs their products and they're uniquely positioned to create them at this point in time. Then in number eight, on the lowest level, we even have great companies today that have immense pricing power. any company that is is specializing in the land power contracts, grid access, construction, I would say even manufacturing companies or construction companies like Caterpillar. That stock is way up because so much so much construction is going on. And again, this is all coming from bottlenecks. Bottlenecks are today what create this immense pricing power for all of these companies. So, as we look through this list, these are the winners today. If you look through any of these companies, these are the ones where all the money is flowing into them. All the investors are piling into these stocks. Uh that we're hitting new all-time highs all the time with these companies. In this phase, this is a period where AI demand grows faster than the world can supply the required infrastructure. In that environment, the best stocks are the companies selling the scarce inputs. the GPUs, foundry capacity, advanced packaging, HBM memory, networking, power equipment, cooling, and data centers. That is squarely where we sit today. Now, many investors may come to the assumption that these companies are so needed today. Their products are so scarce, there's so much insatiable demand for them, their margins and their multiples are going up so quickly that you have to get in on them. You have to own these companies. And to some extent, that's true. It's difficult to be invested entirely out of this entire category because you're missing out on basically all the gains that are happening today and have happened over the past year in the market. But again, this is only one phase out of the next four phases. And I think it's good to continue going over this road map. As we move on, we get to phase two. During phase two, normalization, when supply ends, buyers get more leverage. The sellers into AI demand will not always be the best stocks. There are only the best stocks during the scarcity phase. That's what we're in right now. That's not phase two. That's phase one. During this phase, which is phase two, investors will be primarily focused on the durability of the profits. So, when I look at this, it's all about trying to analyze which of these type of companies have structural changes where they're no longer cyclical and which ones are going to remain cyclical. I believe the most durable sellers are going to be these companies. ASML at the very top. And the reason why is because ASML is not only a cyclical company that sells into this shortage, but they're also a little bit more up on the hierarchy. They sell these massive devices that are installed and then they're used for decades and they have massive service contracts. So, they're not just a company that's selling like memory and it's a one-time sales or a little, you know, a short-term contract. ASML sells big machines used for long periods of time with continual maintenance. And that is why I invest in ASML is because I believe it's more durable seller. My position today in ASML looks like this. It's a $140,000 position with $78,000 in the green. It's already a fairly large position, but I continue to hold every share. And the reason why is because I believe even though you may have questions about the scarcity phase and you you may have questions about these companies, I think you do need to own some of the sellers into scarcity. I think you do need to own some of those companies. Otherwise, you're basically making no gains in this phase. Like, you're just being completely held out of this phase. So, I like having some exposure in this list. I like owning one of these companies so that I can have gains during this time period. Now, ASML, I think, is a very durable seller, but it's also not entirely non-yclical. ASML still have a little bit of cyclicality. Then, of course, we have TSMC. TSMC is a very durable seller. It's not some highly cyclical stock. We have Nvidia which I believe because of CUDA, because of the infrastructure, because of the ecosystem, it has some cyclicality, but I truly believe that Nvidia is becoming less cyclical over time. It is structurally changing to be a more durable seller. Then we also have Broadcom, which again still has some degree of cyclicality like most businesses, but I would say that Broadcom is becoming less cyclical over time. Now, when we get to the companies that I'm more concerned about, when supply eventually catches up with demand, I believe that these ones are far more risky are the most cyclical sellers of the bunch. These include memory stocks, Micron, SanDisk, you name it. The companies that have gone up like 10x because memory is really expensive. Now, it is true that Micron is a great company today. The stock is up above a trillion dollar market cap. Many investors have priced it with a much higher multiple. But it's also true that during any time where a highly cyclical stock historically has gone up a lot, investors start to believe that it's no longer cyclical, that the profits can sustain forever. But I don't really believe that with Micron. I don't believe it with SanDisk. I think that memory companies are benefiting from a one-time massive influx in memory demand, which is likely going to catch up at them at some point. So, I believe that memory companies are highly risky to own. If you own a company like Micron that's trading above a trillion dollar market cap that has these incredible margins, it's good today, but will it be good when the contracts roll out when supply catches up with demand? I'm not so sure. We have data center, construction, power incooling names. I'm very convinced that these companies are more cyclical sellers. They're great companies today. I don't believe they'll be great companies in 3 to 5 years. We have Neoclouds, GPU rental companies. Again, in certain context, those companies are really good. They're making a lot of money today. They're supplying a huge influx of demand today. But I'm not sure what type of moat they have to be great companies in 3 to 5 years when supply catches up with demand. And then we have just a a bunch of companies that are benefiting one time from this. Low margin hardware assemblers. So many of them. These are commoditized companies that are in the right place at the right time, but structurally there's nothing to suggest that they're now durable sellers that will make gains for the next 10 years. None of these companies have robust distribution or subscriptions. None of them have evolved their business model to be on more of an annuity type of business. They're all selling things that are very expensive today because a lot of people want them. And I don't believe that's going to last forever. Phase two will be the most dangerous phase because it will be the separation of the wheat from the tears. The durable sellers, the ones that can really continue to grow their earnings, will do well and then there's going to be some that are proven to be cyclical that will rerate at much lower valuations and investors will lose a lot of money. The important thing here is that the companies selling into all this AI demand will not always be the best stocks. And that's hard to see for investors because you're seeing them be the best stocks today, but they won't in three to five years. The ones that will be the best stocks in three to five years are the ones that can actually use the AI demand and monetize it over long periods of time. That's where we get into phase three. This is where the power shifts back to the buyers. The sellers of AI in phase one are the NVIDIA, the TSMs, HBM, Broadcom, power cooling suppliers, all those companies, the construction companies, the Caterpillars, all of those have the pricing power today. In phase three, which we'll get to, I think in a couple years, the hyperscalers gain power by using custom chips, multiple vendors, internal silicon, scaled purchasing, and owning the customer relationship and demand normalization. they start to take over, take control, lower demand for all the the sellers into AI, but then they have business models on top of that that allow them to monetize customers over long lifetimes. The core AI platforms that I believe will benefit the most in this phase are going to be Alphabet, Amazon, Microsoft, and Meta. Now, when I look at Google, Google's one of these rare cases where they're kind of in phase one and they're kind of in phase three. Part of the reason that Google stock is so high is because of their custom TPUs. That's the reason it's going up today. But I believe that Google will go up even more as we get into phase three. And they show that they can monetize these customers over long periods of time with their massive distribution. See, in phase three, when the power shifts to these buyers, it's because these buyers, these hyperscalers have tools to be able to infuse AI into all their products and then monetize it for long, long lifetimes. Microsoft will have Azure C-Pilot, GitHub, Office Security, Enterprise Software, and on and on and on. That could go on for like 10 minutes listing the the different ways Microsoft can monetize AI. With Google, we've already seen it. We've seen Search, YouTube, Gemini Cloud, TPUs, Ads, Enterprise AI, and on and on. Even things like their new products, the Fitbit Air is using AI to monetize an existing product. It turns a lot of vitals into like takeaways. Uh it's incredible the the different tools these companies have to monetize AI. But remember, we're in phase one. We're not in phase three. In phase one, all these companies are dishing out lots of cash. All the buyers are dishing out cash, making their metrics go down and making all the sellers into AI have immediate earnings. So these companies are putting out cash flows. Cash flows are going out. All the phase one companies today are making earnings. Over time, these companies will be able to use all that cash that they outlaid. They'll advertise it and then they'll profit with these with these tools and all the investments they've made for the next 10 to 20 years. So, you're looking at a long lifetime of monetization. Amazon is doing this through AWS, Tranium, retail automation, ads, logistics, AI services, shopping assistance, and so on and so forth. There's so many ways that Amazon's monetizing AI. With Meta, we have ad efficiency, recommendations, AI systems, business messaging, content generation, wearables. There's another hundred ways that they're using AI to monetize for long periods of time. These stocks really haven't done too much this year. Most of them haven't been that good of investments over the last year or so. Google's really the only standout that's gone up a lot. And part of the reason why is again because Google is part in phase 1 because of the TPUs and part in phase three. But I really believe once we get over this next year or so, once these sellers into AI start to lose power, investors are less focused on on these companies and owning these companies and supply catches up with them, a lot of the attention will start to shift back to the companies that have the long-term durable relationships, the ones that have distribution, subscriptions, all the different tools, all the the different things that people interact with on a daily basis. That's these companies. Everybody's interacting with Amazon, Meta, Google, and Microsoft every single day. They're the ones that own the customer. They own the lifetime relationship. So, this is going to be a big power dynamic shift that will happen over the next 2 years. I want to reiterate that this doesn't mean that every company from phase 1 will do poorly. And I also want to reiterate that I think you should own some companies from phase 1. For example, I chose ASML. I wanted to have some foot in what's going on today. I think that Google is part phase one as well again, but I think that ASML will continue to do well. I think TSM will. I think Broadcom probably will and I think Nvidia probably will. Those companies will likely do well, but there is a huge risk of these phase 1 stocks that these AI sellers will rerate much lower as this power dynamic shifts into the buyers. Now, part of this overall transition, we have to look at software stocks. They have in most cases imploded. the valuations and multiples have been completely reset or rerated much lower which means a lot of companies that were trading at very high multiples into the 30s are now trading into the teens. The stocks are down 30 40 50 60% sometimes even more and it's not going to be that way for these stocks forever. This is where we get to phase 4. Phase 4 is when software winners start to emerge. To summarize this, I believe that after the power dynamics start to shift, we'll also see some dramatic changes in software. As AI compute gets cheaper, software should be split into two groups. Some companies will be rerated higher because AI makes their products more useful, more personalized, and more profitable. These are the companies that own distribution, proprietary data, customer relationships, workflows, and our systems of record. And the companies that have more of this are the ones that are going to be rerated higher. They're the ones that can protect their mode. But during this process, other software companies will be permanently commoditized. If the product is mostly just a UI feature, a workflow shortcut, the AI agents, AI agents can copy, bundle, or bypass, the old software layer may still exist, but investors may assign it a permanently lower multiple. Predicting which ones will end up resurging and which ones won't is difficult, and there's risk here of being wrong, but here's my take on it. I believe the more predictable winners are these ones above, Google, Microsoft, Amazon, Meta. I just think that they're winners. They have so much distribution. They have so much customer lock in. You know, they they face risks to varying degrees. Google has to compete with chatbt. Microsoft has to deal with claude within its business. Uh Amazon, I think actually Amazon is in a great position. Amazon and Meta are my two top picks this year. But overall, I just view these as predictable winners over the long term that will eventually have their day in the light. That's when phase one and phase 2 come to a conclusion. We also have companies that I believe still have the distribution, the longevity, the customer lockin, the unique data sets, all the all the stuff that will make these companies not commoditize. That's S&P Global, Moody's, Faxet, Msei. We also have companies that are at some risk in some aspects of AI, but overall they have a lot of nonAI aspects, and I'd put Uber and Door Dash in that category. I think Uber and Door Dash will be spectacular winners. I think that Shopify is a spectacular winner. I think that Airbnb will do really well. We even have companies that there's a bit more debate about companies like Spotify and Dualingo. They don't own proprietary data per se. Spotify just has access to music. Dualingo has access to AI curriculum and courses. But because of learned behavior, people use Dualingo mostly for the motivational aspect of it, the scores and streaks and social aspects more than just the content itself. So I believe that those will end up being differentiated and be rerated higher as well. when we get into the less predictable ones. Now, the reason I say that these are less predictable is because I really don't know how these ones are going to turn out. They might do well, but I'm really not confident in any direction. I think that Docusine is at significant risk. This company's major product is simply e signatures and I believe that there's massive bundling risk. Like Adobe's coming after DocYsine, we have Microsoft, all these different startups that are offering signaturebased documents. what they do is not technically difficult anymore. A lot of smaller businesses can create the same thing and bundle it into their products. And I think that's a real concern for DocYsine. We also have the same thing with Zoom. I just see that Zoom is in a a very difficult spot. There's so much bundling risk with it with Microsoft Teams and all these different companies that offer very similar uh features. Uh we have Salesforce, Adobe in it, Autodesk and generic SAS and AI rappers. Now, with Salesforce, Adobe, in it, and Autodesk, again, I don't know for sure if these companies will do poorly, and that's not what I'm saying here. They could have a big resurgence. They could rerate higher, but I just believe that they're far less predictable than the companies above. AI is targeted more specifically at these businesses. It is targeted as a threat for these companies. When I look at this overall, I'm trying to have my portfolio mostly positioned in the companies that I think are the more predictable winners. And this is how I'm positioning my strategy over the next five years. Again, right now for phase one, ASML is doing its work. It's going up every single day. ASML is currently up 39% year to date, and it's up 113% over the past year. It's trading like one of these sellers into the demand. It's doing exactly what I expect it to do. It's providing me gains throughout this year while we're in this phase. Now, what I don't want to do is get greedy and start to buy all the companies in this phase. I'm not buying SanDisk. I'm not buying Micron. I'm watching these companies going up knowing that this dynamic won't last forever. So, I'm being patient here. I don't mind having part of my portfolio in these companies. And whether you chose ASML or TSM or Broadcom or what have you, as long as you choose one that likely has a highly durable revenue stream, it's not as cyclical and won't revert back to cyclicality in the next 3 years, I think you're going to do okay. But I think you should have some exposure to phase 1. But where I have most of my exposure and where I believe that the long-term predictable gains mostly reside are in the phase 3 winners, the buyers of AI, specifically Google, Microsoft, Amazon, and Meta. I have made these four companies in particular the biggest bets in my portfolio. Not Tesla, not Nvidia. It's Google, Microsoft, Amazon, and Meta. All the hyperscalers are the companies that are buying the AI the fastest. I have Microsoft in the passive income portfolio with $70,000 invested. Google $130,000 invested. Both of these are are massively in the green. We have Meta as a brand new position this year that I've already put $180,000 in. Meta is now my third largest position. Then in the story fund, we have Amazon as a $188,000 position. We have more Google, another $90,000. Most of its gains in this portfolio, but I continue to hold every single share. We have Microsoft, an additional 21,000. The other companies I think are not quite as predictable, but I still think very good are S&P Global, Moody's, Fax, SetET, and MCI. Out of these ones, I've personally chosen S&P Global and Moody's. These ones have been under pressure. A lot of investors are concerned about them, but I still remain very bullish on them. I own over $100,000 of S&P Global, another around $47,000 of Moody's, and I still believe these ones will be big winners. To put it simply, I do have direct exposure to what's going on today. That is the ASML and Google holding. But over the long term, I am optimizing my portfolio and my investments for what I think will be the most durable winners over a long period of time. The ones that will have that lifetime relationship with the customer. They'll be able to use AI to benefit their their monetization, to benefit their efficiency, to benefit their margins. Those are the big tech companies. Those are the ones with the proprietary data. And that is where I'm concentrating my portfolio into. And I think it will take about a year or two to see these investments really pay off. Now, let's go ahead and move on to some news. Now, the first bit of news that we get to are these headlines about Ferrari. Ferrari just released its first EV. Now, it gave people like a a preview of it. Now, it's finally been released. And the market is actually upset with this. Investors are trading the company down. It's down 5.7%. So, some investors are deciding to sell out of the stock. And what is wrong with the Ferrari EV? Well, first thing is just the looks of the car. Like, this is the new design for the Ferrari EV. One of the problems is it just doesn't look like a Ferrari. Like it completely lost the aesthetic. In fact, I think if you did a test where you just took the logos off of this, it'd be very difficult to tell if this is a Ferrari or any other Chinese EV. Like there's so many vehicles that look very similar to this. You have to have the logo on to even know what car it is, and that's rare. Ferraris typically have their very unique design. It says, "The highly anticipated model marks a departure from the aesthetic of the typical Ferraris that come even as other luxury car manufacturers, notably Porsche and Lamborghini, have scaled back on plans to launch their own EVs due to weak demand." Now, they're asked about this because they they know the backlash. They have to pay attention to all the social media content. They say when asked whether the company could satisfy both new customers and its typical clientele, they said look when you do a new technology you need to always to keep in mind a word that is called respect. Respect of the technology because when you have a new technology you need to make sure that the technology is properly presented in the design. So the design must be different. Okay. So they're saying now that they're powering I'm trying to decipher what this is. This is one of the most convoluted ways of making a point, but basically they're trying to respect the design or respect the new technology, which is EVs, electric powered instead of gas. And to respect that, they have to make the design look very generic, like a generic plastic toy car. The car maker also respects the different needs and wishes of its customers, adding that existing clientele will be interested in the loose and the company will welcome new buyers thanks to the fully electric model. So, they're trying to grow their TAM without offending current buyers of Ferrari. But I believe this is a a big problem for Ferrari, bigger than I think some investors are even giving it credit for because you can't just be Ferrari, a company that's known for brand. That is your company. It's brand. Anybody can create a car that goes faster than Ferrari or looks better than Ferrari, but it doesn't have that Ferrari brand along with it. What makes Ferrari truly notable is the brand that they've carefully cultivated over decades and decades. It's a brand that carries so much history, rich history with it. It's a brand that has such exotic designs that are very unique that that's what makes people want to pay fortunes for it. They want to pay way more than anything else that's even comparable. When you come out with something like this and you say, "Hey, current Ferrari buyers. We're just making this for new people. This is just for new clientele. We have other cars cooked up for you." You You can't just separate the two. You can't pretend this doesn't exist and that your current buyers are just going to ignore it and they're going to buy the nicer ones. This does affect the brand. By making a cheap and downed EV version of your car, it certainly affects the brand and aesthetics and notability of your other vehicles that you're selling to your higher priced clients. So, I believe this really does represent a a problem for Ferrari. They need to find ways to try to advance their brand and move into EVs. But the truth is that EVs are just not as cool. They're just not as cool as their old vehicles. They're they're kind of cool in a different way. You know, you have Tesla and they can make new designs and they're very quiet, but part of Ferrari is that rich, vibrant history that is so notably part of the engine. The engine plays a huge part in the brand of Ferrari. The roar when you start up the vehicle. When you take away that, it's just completely different. It's completely different. It's definitely something that affects the brand. I think this is going to be a struggle for Ferrari to deal with over the next decade ahead. Now, moving on, we get to today's fail of the week, which in this case are the people suggesting that the Colbear Late Show was cancelled because of Trump. Now, this isn't a crazy suggestion. After all, President Trump makes himself the center of everything. He's in some cases very loud, almost obnoxious, and he's taken to attacking the late night show hosts. He doesn't like them. He doesn't like Jimmy Kimmel. He doesn't like Jimmy Fallon. He doesn't like Steven Cobear. He doesn't like any of them because, of course, they make fun of him. For years, the late night shows have made their primary target for ridicule the president. And that's part of being American. You can mock and ride the president. In this case, President Trump has hit back. He's made fun of all these show hosts. He's said that they're failures and whatnot, and it's created this back and forth between the two. And then the show gets cancelled. A lot of people believe it was because of the president. But there's another factor here that is just missing from this analysis. Uh it's clearly just YouTube. That is by far the reason that Coar show was cancelled. It's because of YouTube. YouTube has crushed traditional TV and it continues to crush traditional TV and it's not even particularly close. When analysts looked at this TV show, they cited financial losses of around $40 million annually. Former CBS executive David Refield noted that the total late night network revenue has halfed in less than a decade from $440 million in 2018 to around $200 million. So, you have a show that is now losing $40 million annually and they're actually projecting those losses to go up to increase. They say as younger viewers migrate to digital platforms, they have high production costs, they have large staffs, they have declining advertiser interests, it's made the format increasingly unsustainable. Even with aggressive cost cutting, it's unlikely to reverse the trend. See, the problem for these shows is not Trump. And it's easy to blame Trump for everything, but in this case, it's purely YouTube. YouTube is the big problem here for late night television. We can also look at another, I think, really revealing piece of data here. This was shared from the Late Shows Twitter account. They posted this and they said, "We're saying goodbye to all the staff. They're going to have to find new jobs or work on new shows." And this is what they showed. That's a lot of people for a single show, a nightly show where you have celebrities on. Plus, they have the whole band in the mix here as well. The overhead for this show was like a hundred million dollars per year to produce this show ongoing every single night. And the show itself is getting a couple million views per episode, which is similar to many low-level YouTube channels that don't have production costs at all. There's many YouTubers that just get on and start talking about things and get a couple million views without having a hundred people work on this show. This model is just dead. It is just completely dead. And it's not just Steven Colbear. The Seth Meyers show recently got rid of the band. So when new guests come on the show, it's just like speakers playing music and they just come and sit down. There's no live band. They're cutting down costs aggressively to try to keep the Seth Meers show on. The Jimmy Kimmel show right now is reportedly profitable, but barely profitable. And they've had to do aggressive cost cutting as well to make that one work. This is a problem for every late night show. Audiences have moved to YouTube. They know that they don't have to watch an hourong show where a couple celebrities they've never heard of come on and talk for a bit. They know that if anything is even remotely interesting from those shows, it'll just be clipped and put on YouTube anyway. So, they'll end up seeing it without having to bother with all the ads or looking through the entire show itself. The model itself has completely changed and you're seeing it change in all the other ones. In fact, Bloomberg's analysis here argues that Trump made these shows last longer than they would have otherwise lasted by making them more culturally relevant by constantly attacking them. He made them have some type of united front against Trump, which is a theme that kept the shows alive for longer than expected. But in any case, the dominant force here, the dominant change is YouTube. And you're seeing this happen in real time. YouTube will continue to consume traditional television. It has been happening for years. It continues to happen. And you'll see these other late night shows eventually downgrade, massively cut budget, and get cancelled as more and more of it shifts to YouTube. And I would bet in the coming year or so that Steven Colbear will be back on the air, but this time with the YouTube model, but we'll have to wait and see. That's it for this episode. Hope you enjoyed. See you in the next one.